By Ian C. Schick, PhD, JD, CEO & Co-founder of Specifio (first posted on blog.specif.io)

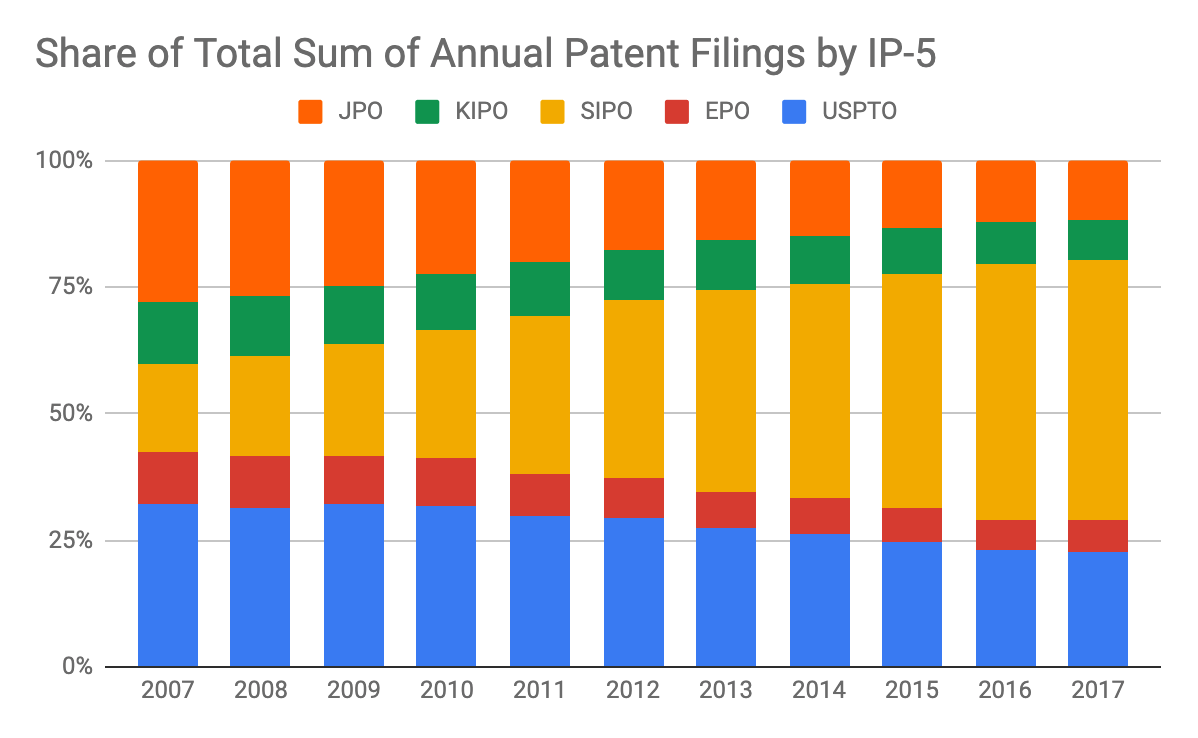

In our previous blog post, we explored how annual patent filings may be an indicator of optimism towards the strength of a jurisdiction’s patent system and its underlying economy. This article picks up the analysis to shed light on the effects of resident status on filing behavior over the past decade among the top five patent markets–US, China, Japan, Europe, and Korea–known as the IP-5.

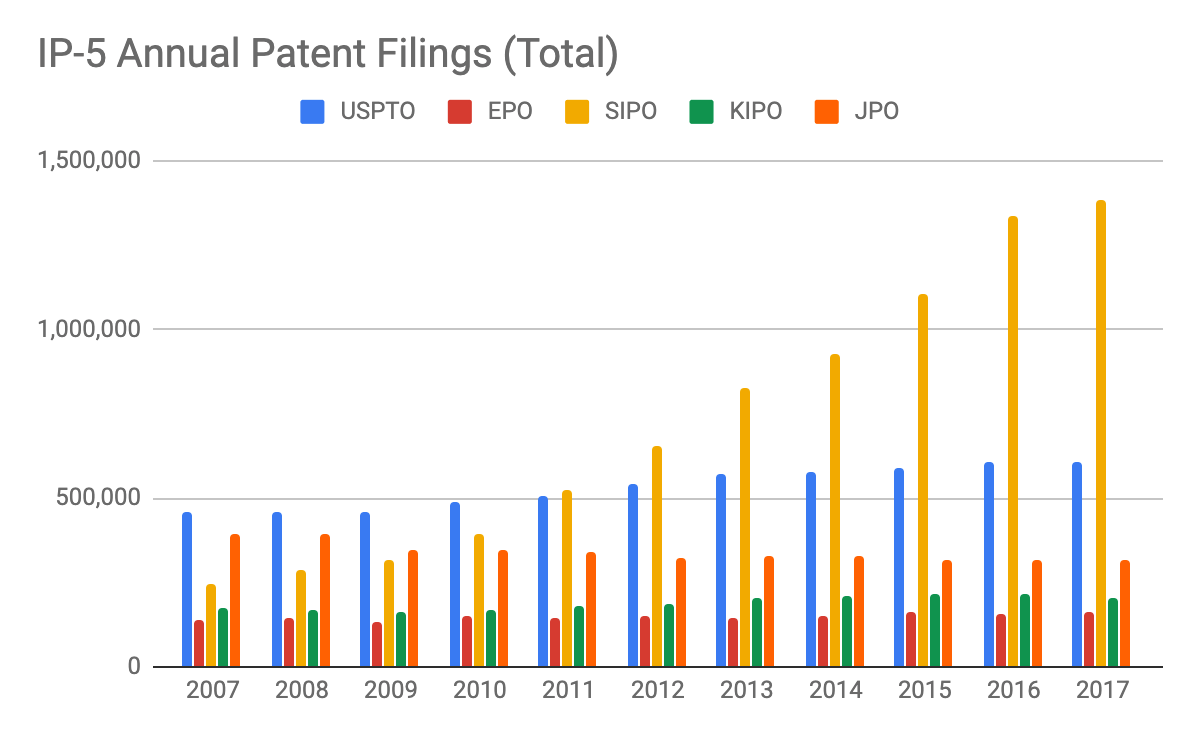

The graph below shows the total number of patent applications filed each year in the IP-5 jurisdictions, with non-resident and resident filers aggregated together. At a glance, filing activity appears relatively stable with modest changes, at least compared to the rapid ascent and shear volume of Chinese patent filings.

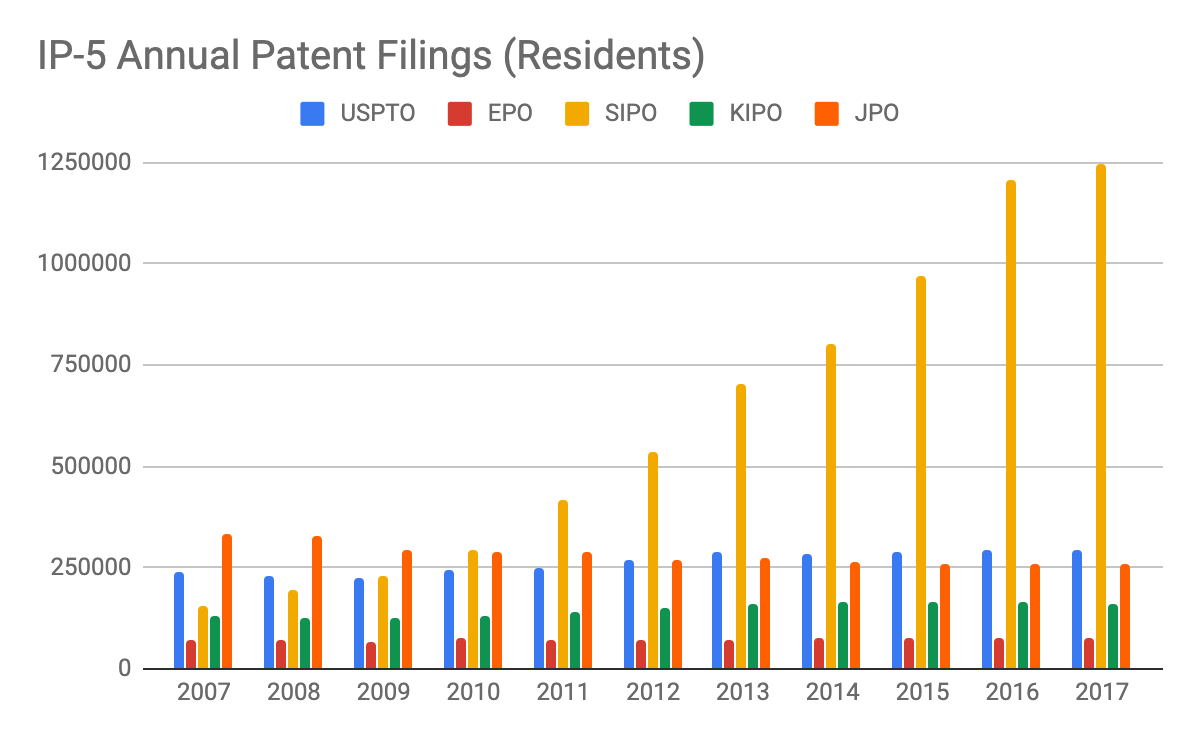

Separating resident and non-resident filings shows interesting differences between the two categories of participants in each of the economies of the IP-5 jurisdictions. The graph below shows the number of patent applications filed by residents in each IP-5 jurisdiction.

In China, a hugely disproportionate amount of patent applications are filed domestically. In the last decade, 85% of patent applications filed with China’s National Intellectual Property Administration (CNIPA; shown in the figures with the former name, “SIPO”) were resident-based. From 2007 to 2017, China’s total number of domestic patents equaled 6.74M, which is roughly the same as the resident output of the U.S., Europe, and Japan combined. It would be interesting to see how this dramatic increase in filings has affected the number of those practicing patent law in China.

China has boosted domestic patent production though a number of initiatives. The country has seen significant investments in innovation, such as artificial intelligence. Also, there are patent-promoting policies, such as subsidized patent filing fees, rewards for patent filings, and tax credits related to patent output. China has assuaged examination guidelines for software and business methods patents and streamlined the examination process for rapidly expanding sectors, such as cloud, big data, and internet.

While Japan’s resident fillings have fallen, South Korea, Europe, and the U.S. have seen steady increases, suggesting a possible correlation with the positive economic activity of these jurisdictions. In the last decade, Japan’s resident patent filings, however, have steadily decreased by more than 20%, which may be explained by a sluggish national economy struggling to get back on its feet.

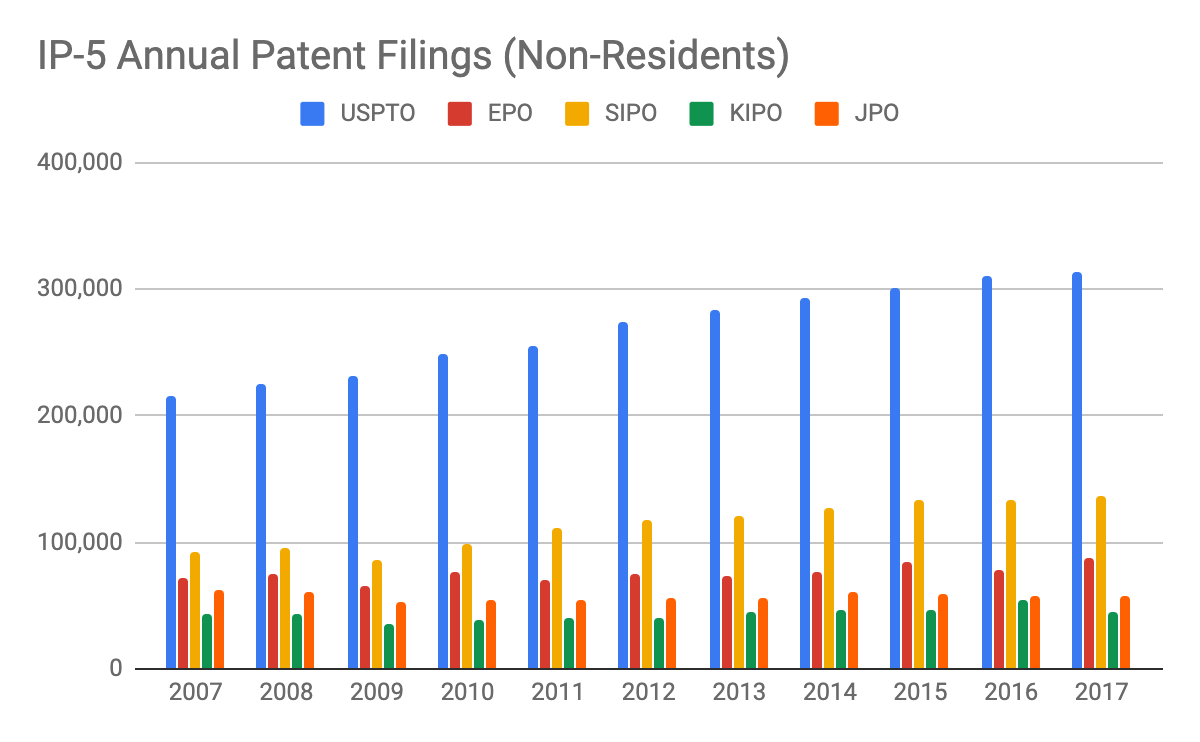

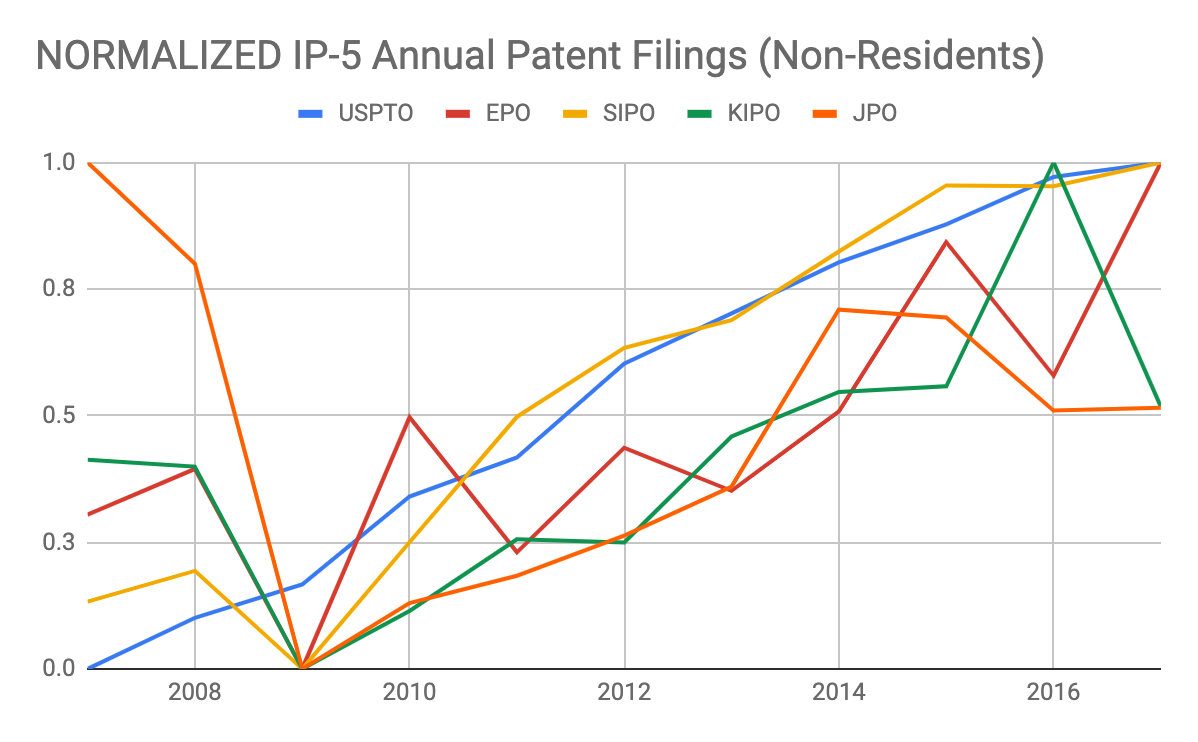

The graph below depicts the number of patent applications filed by non-residents for each IP-5 jurisdiction.

As illustrated above, the United States Patent Trademark Office (USPTO) is clearly the most popular destination for non-resident patent filings. For almost every single year in the last decade, more than half of the applications filed with the USPTO were of foreign origin. As the largest economy in the world, it makes sense that entrepreneurs and inventors want to file patents in the U.S. Due to the thoroughness of American patent law, the U.S. offers arguably stronger patent protection than other countries or regions.

Similar to the U.S., Europe has significantly more non-resident than resident patent filings, which may be due to the same reasons mentioned above. The U.S. and Europe have the most balanced production of domestic and foreign patent filings. The Asian market, on the other hand, is dominated by domestic patents. In the last decade, non-resident filings made up less than a quarter of total patent filings for China (15%), Japan (20%), and South Korea (23%).

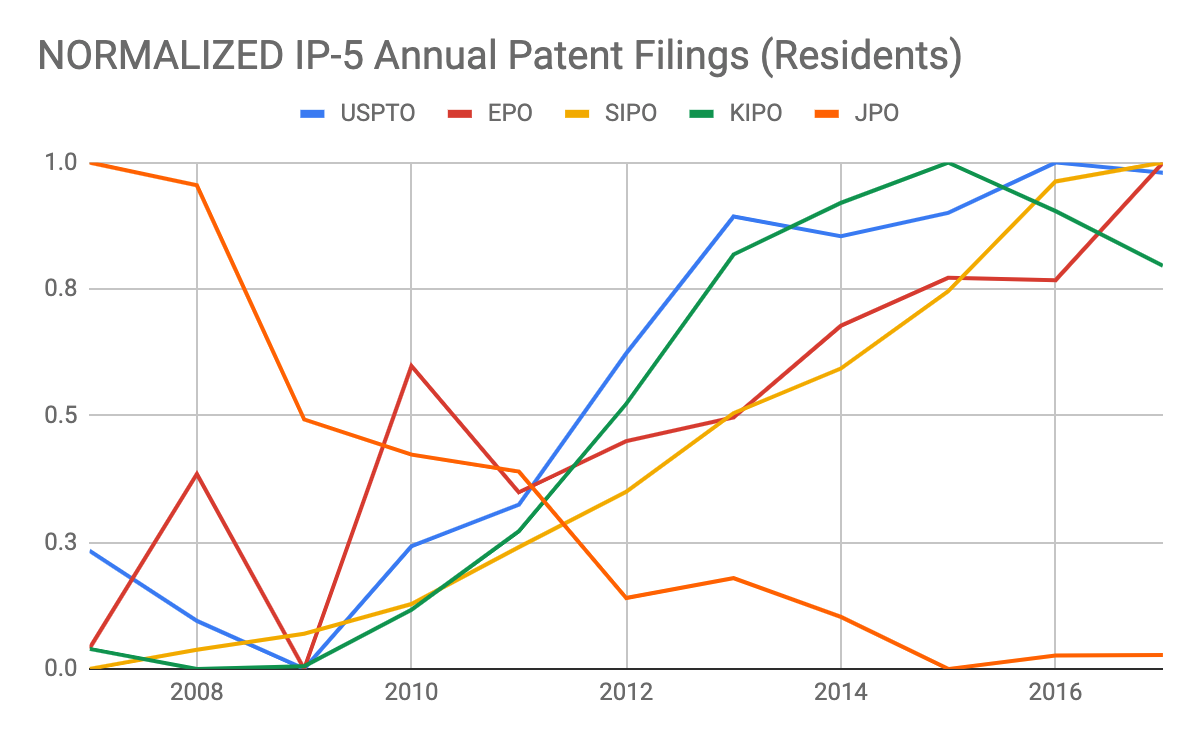

In the plots below, resident and non-resident filings have been normalized to more easily compare the “shape” of the filing trends. This graph has been created so that maximum annual filings over the past decade are scaled to equal to one, while the minimum is scaled to equal zero.

It appears all IP-5 jurisdictions, except China, took a significant dive in 2009 with the USPTO, EPO, and KIPO hitting a local minimum. Japan’s steepest fall was from 2008 to 2009, but its patent filings did not bottom out until 2015. U.S. resident fillings also saw a dip in 2014, which is presumably due to the Alice and Mayo cases that cast doubt on the patentability of certain fields of innovation. It is not immediately clear what factors caused the volatility in Korean resident filings.

We see above that foreign filing entities maintained confidence in American patents through the economic crisis and the Alice-Mayo fallout with barely any fluctuations in steady year-after-year increases. Non-resident filings among the remaining IP-5, however, hit a low in 2009, but have mainly risen since.

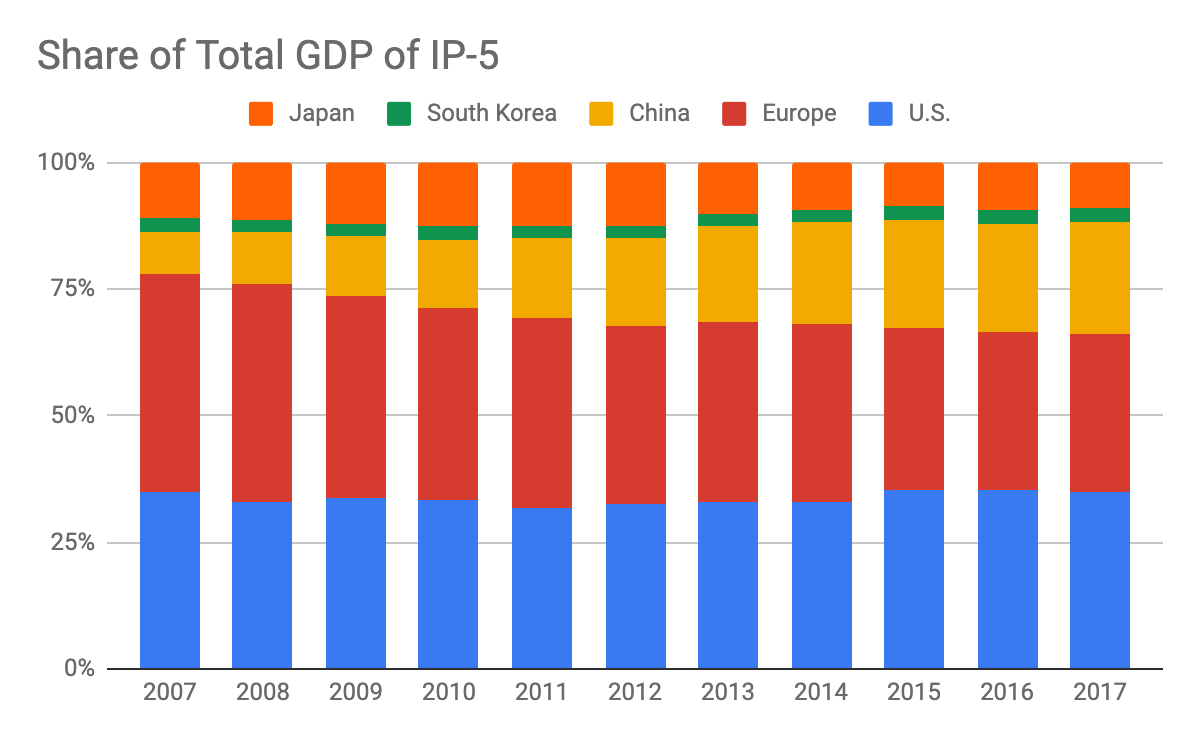

The U.S. and China are the clear favorites in the international patent market, but in different ways. China is a mass-producer of domestic patents in part due to their favorable policies and incentives, while the U.S. has maintained a more balanced approach with a healthy influx of foreign patents. By integrating resident and non-resident factors into this analysis, we have gained deeper insight into the productivity and health of each jurisdiction, as well as the sensitivity of the overall market to external factors. Although Europe is the smallest producer of patents among the IP-5, they are still known for having one of the highest ratios of foreign-based patents, which is a testament to their strong patent system. It will be interesting to monitor the production trends of these different countries moving forward and whether they decide to take a quality or quantity approach in production.

So what does all this mean for practitioners? We see above that diversifying clientele to include non-resident U.S. patent fliers and resident Chinese patent-filers could help weather economic downturns, which more often is followed by dips in patent filings. Furthermore, In order to chase Chinese patent work, practitioners’ best chances may be to develop business among Chinese resident filers.

Data Sources:

- Increases in Innovation, Patent Boom Leads to Development in China http://www.ipwatchdog.com/2018/04/18/increases-innovation-patent-boom-development-china/id=95994/.

- Annual Patent Filing Data for IP-5 (2011-2017): IP-5 Statistics Report 2011-2018, Four-Office Statistics Report (2008 – 2010), World Bank Indicator https://data.worldbank.org/indicator/IP.PAT.NRES, and WIPO Statistics https://www.wipo.int/ipstats/en/statistics/country_profile/profile.jsp?code=CN.

Featured on: